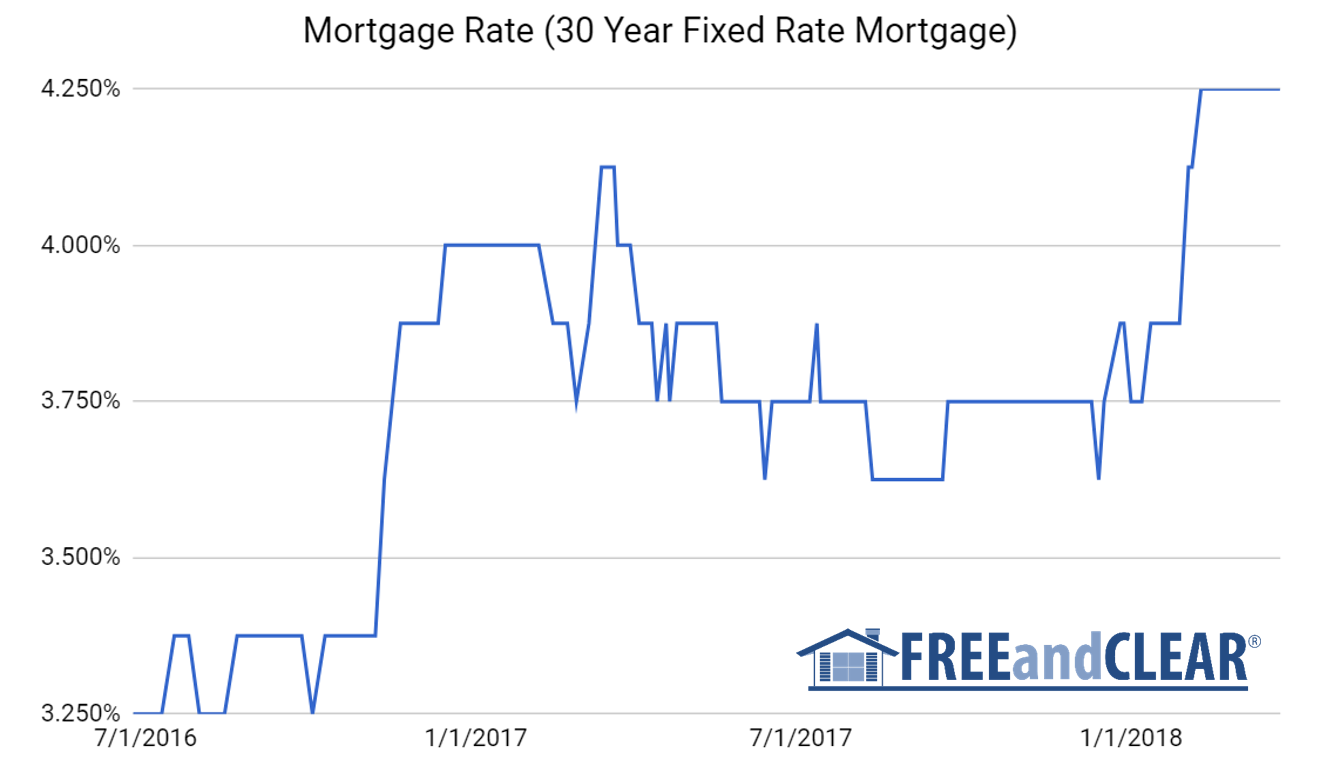

Last week the Federal Reserve raised the key Federal Funds rate 0.250% to 1.500% to 1.750%. The Federal Funds rate is an important interest rate that affects borrower costs for many banks and mortgage lenders. When the Federal Reserve raises interest rates, mortgage rates usually go up but that did not happen after the Fed’s announcement. In fact mortgage rates were flat or even down for some lenders after the Fed released its statement. Why would mortgage rates go down if the Fed increased rates and what does this mean for mortgage borrowers?

Last week’s events underscore multiple important lessons about mortgage rates. First, market expectations are one of the most influential factors that determine mortgage rates. The Federal Reserve had telegraphed its rate hike for almost a quarter so the rate increase did not surprise many lenders. Most banks and lenders had already included the Federal Reserve’s interest rate hike into the price of their mortgage rates before the Fed released its statement, which helps explain the lack of reaction to the news by mortgage rates. We can assume that mortgage rates would have responded much differently if the Federal Reserve increased the Federal Funds rate more than expected or if they adjusted their outlook for future rate hikes, because this news would have run contrary to mortgage market expectations.

It is also important to recognize that the Federal Funds rate is not the Fed’s only policy instrument. The Fed has the capacity to buy investment securities such as bonds and other debt instruments to apply policy initiatives. In the aftermath of the most recent recession, the Federal Reserve bought hundreds of billions of dollars of mortgage backed securities and other debt to help stabilize mortgage rates. Although the Federal Reserve has communicated its plan to reduce its mortgage backed securities holdings through periodic sales, it may also buy mortgage backed securities to support the market when needed. So the Fed may implement policies in addition to changing the Federal Funds rate to promote mortgage rate stability.

One last point to emphasize is that although the Fed is a key factor in determining mortgage rates, there are other inputs as well. Additional factors like bond pricing, treasury yields and the equity market also impact mortgage rates. For example, the day following the Federal Reserve’s announcement, the stock market dropped significantly in response to fears over a possible trade war. In a flight to security and quality, investors sold off equities and purchased bonds and U.S. treasuries, which caused debt yields to decrease. Bond and treasury yields are a key determinant of mortgage rate pricing so when yields slip, mortgage rates usually follow suit. So in some ways, trade tariffs are indirectly responsible for keeping mortgage rates steady.

The bottom line is that in the near term, mortgage rates are very challenging to predict. The Fed increased the Federal Funds rate, but mortgage rates were steady or even down in some cases. Market expectations, debt yields and many other factors cause fluctuations mortgage rates daily or even hourly and mortgage rates may not always react to the Fed’s moves.

In the long run, however, mortgage rates typically find it hard to resist the Fed. So while we may have been surprised that mortgage rates dropped moderately after the Fed’s announcement, it was likely a temporary reprieve. With the Fed reinforcing its outlook for two more interest rate increases in 2018 and possibly four rates increases in 2019 we should anticipate that mortgages rates to continue to rise over the course of the two years, even if their upward trajectory is not always straight.

So while it is impossible to predict mortgage rates, Fed policy typically wins over the long haul. The next time the Fed increases the Federal Funds rate, we may not be able to count on a possible trade war to keep mortgage rates steady. In light of this dynamic, potential home buyers and borrowers looking to refinance may benefit by locking in a mortgage rate sooner than later.

This article first appeared on FREEandCLEAR. For free mortgage resources and rates please visit FREEandCLEAR.com.