From mortgage preapproval to your home warranty, this homebuyer's guide will help you find the home of your dreams and set your expectations for the process. This isn't a check list, take out a piece of paper (get your spouse if necessary) and use this guide to jot down your path to homeownership.

What's in this Guide:

- Is Homeownership Right for You?

- How to Evaluate Yourself Financially

- New Construction Home or Resale Residence?

- What Type of House is Best for You and Your Family?

- What Features/Upgrades do You Want in Your Home?

- How Much House Can You Afford?

- Find the Right House for Your Life

- Compare Financing Options

- Getting Your Downpayment in Order

- After the Purchase

Is Homeownership Right for You?

Purchasing a home is a significant financial and personal commitment. It's not always a good time to buy a house, and the market should not influence your purchase.

Before spending much time looking for homes, it would be best to ask yourself these simple questions. Remember, it's better to wait until you are ready to own a home than rush into the commitment without logically reviewing your finances.

Do you plan on moving in the next five years? Are there any significant life changes coming up that may affect your work or job? Can you afford home maintenance and the cost of house repairs? Are your employment and income stable? Do you live below your means and save money? Are you an accountable person?

How to Evaluate Yourself Financially

As we mentioned above, home buying involves a significant financial commitment from you. It's also a commitment from your lender and sometimes taxpayers. Make sure your finances are in order before comparing financing options and applying for prequalification.

Add up your monthly income; if you have a spouse or partner, add their income too. Review account statements, add up all debts, list any other obligations and create a monthly budget (if you don't already have one).

What did you learn? Do you have extra spending money each month? Do you already save money and have a downpayment? Can you afford an emergency after you buy your home? Will owning a home make it hard for you to save money?

Look at each credit card account, and look at each bank account over time. Fact check yourself and ensure that you are financially able to own a home.

The purpose of all this thought and work is to get prepared for financing and homeownership. Having these documents in hand and knowing how much you can afford will help you make a prudent decision about buying a home.

New Construction Home or Resale Residence?

Do you want a new house, or are you looking for something already owned? Buying new vs. resale could affect a few aspects of your home search. If you know you want something you built, something never lived in; then a new home is for you.

Suppose you are looking for something in the city or an established neighborhood. In that case, it's probably ideal to hire a real estate agent. Their expertise will usually help with several different parts of the process and end up saving you money.

On the other hand, if you are looking for a home outside a major city where new home developments are, you probably do not need an agent. Agents are excellent, but home builders typically offer more than enough resources for homebuyers.

What Type of House is Best for You and Your Family?

You generally have several different home options in most cities. Make sure you consider your lifestyle and how you want it to be when buying a home.

There are condominiums, attached triplexes, duplexes, and townhomes that offer low maintenance. There are active adult homes tweaked out to make it easy for aging adults. And there are single-family homes and estate homes, which would offer an entirely different lifestyle than a hi-rise downtown.

It's worth taking the time to identify and talk about the home you want to own. List the pros and cons. Talk about everything with your family.

Keep in mind that an agent's expertise will come in handy for more unique purchases. Plus, if you want to save a little money by buying a house you can fix-up, an experienced real estate agent may help.

What Features/Upgrades do You Want in Your Home?

This specific portion could be ten pages long, but we'll keep it short. You are making a significant - long-term decision. It is vital that you consider what you want, especially if something, in particular, is crucial.

Be sure to think of everyone living in the family and have an open discussion. Discuss your kitchen, bathrooms, and exterior areas. Talk about the bedrooms and closet wants and needs. Discuss the nice to haves and the must-haves.

Take note of essential items from the discussion.

How Much House Can You Afford?

Everything discussed until now needed to take place before we could figure out what we could realistically afford. The downpayment, extra amount you can save per month, your features - the must-have items and the nice to have things, even the real estate agent.

Given the information you now have. Plus the fact that experts widely agree that your mortgage should never exceed 28% of your gross income, how much home can you 'really' afford? What kind of home and where? Use the 28% rule to stay safe.

Let's say you and your spouse gross $5,000 per month. In a perfect world, your mortgage would be less than 28% of that number.

5,000 x .28 = 1,400 - in this example, you can afford a home that costs $1,400 or less each month.

If this is you, your mortgage payment shouldn't exceed $1,400/month.(principal, interest, and taxes)

Whatever your number is, you'll need to sit down and figure out precisely what you can afford. Be realistic, even conservative. Worse case, you'll figure out how much money you need to save and earn to one day become a homeowner.

The best-case scenario. You make the entire home buying process smoother, and you enter the process with proper expectations.

Find the Right House for Your Life

You've put in the work and know what type of home you want, the features and upgrades you want, and you know what you can realistically afford. You can stretch your dollar further by comprimising in a seller's market. If you're buying new, KitchenAid appliances and outdoor kitchens come included with some luxury homes.

You already know the home type, the features you want and all the other items.

Now's the time to start searching for your dream home! If you think you'll hire an agent, then start by interviewing them.

If you're going to look for a home on your own, the Internet has everything you need to get started. There are niche websites with new home resources and builders, new home listings websites like RedFin with price estimators, blogs with tons of great information, review websites about companies and builders and many other online resources for homebuyers.

Start online, compare homes and widdle your way down to that gem. This step and the steps below will be going on simultaneously until you decide on a home and lender.

Compare Financing Options

After you've figured out all of the above, you are ready to get started comparing your financing options. It's time to get referrals and start meeting with professional lenders and mortgage brokers. Get multiple offers, ask questions and make sure you understand your choices.

If you're buying new, consider that some builders can pay builder closing costs if you use their preferred lender. If you're buying a new construction home, this is certainly worth considering. It's usually a percentage of the home and when luxury builders do it, you can save big!

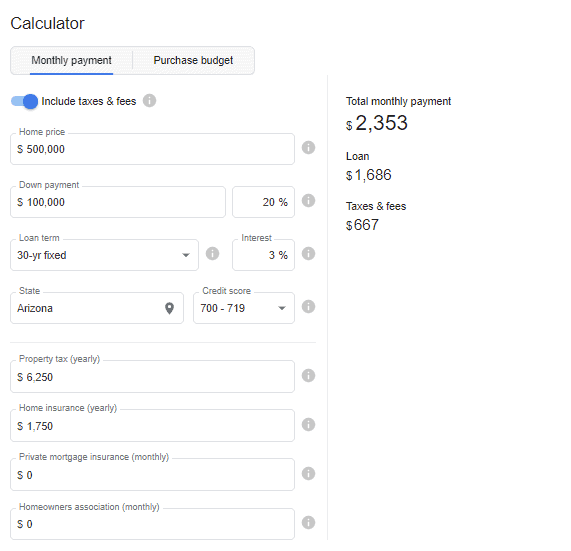

The cost of a $500,000 home with a 20% downpayment of $100,000 or a loan with a principal mortgage of $400,000. Fixed rate of 3.5% over 30 years.

$2,353/month

(total monthly payment)

Source: Google Calculator

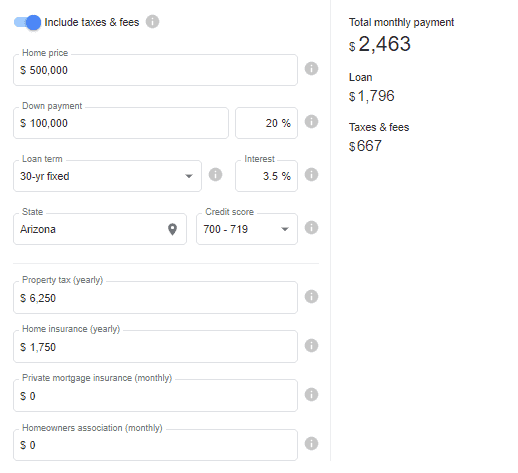

The cost of a $500,000 home with a 20% downpayment of $100,000 or a loan with a principal mortgage of $400,000. Fixed rate of 3.5% over 30 years.

$2,463 (total monthly payment)

Source: Google Calculator

Pro tip: Over 30 years, on a $400,000 mortgage, you will save roughly $39,600 with an interest rate of 3% instead of an interest rate of 3.5%. Interest rates are important, which is why many experts urge buyers to purchase a home before interest rates increase.

Getting Your Downpayment In Order

The amount you'll need for a down payment depends on the home's cost and the loan type. You should put down as much as you can afford.

FHA loans require as little as 3.5% down, but you may also have to pay for closing costs, and there are fees associated with getting the loan and title. Conventional loans require a downpayment of 5%; some lenders want 20% down. Conventional loans also have costs for financing.

Take the time to make sure you have your downpayment in order. If you buy new, the home builder may require a deposit to start construction. Ensure you have the downpayment and other money accessible before bidding on a home, especially in a seller's market.

After Your Home Purchase

Understand Your Warranty and Documents, Save them

If you buy a resale house, check if you can transfer any of the original structural warranty to you from the builder. In most cases, builders offer a 10-year structural warranty on the home and between 1 and 2 years on appliances, smart features, and other upgrades.

Your warranty situation will be unique, but make sure you look into your options and understand them. Get home owner's insurance and anything else you need.

Take it from us. You'll need different paperwork over the years. Store it all, your title, mortgage paperwork, insurance documents, vendor information, warranty details, and anything else in a fireproof safe at home or your local bank.

See Also:

Zillow's Free Nationwide Mortgage Calculator - https://www.zillow.com/mortgage-calculator/

Tips for first-time buyers - https://www.nerdwallet.com/article/mortgages/tips-for-first-time-home-buyers