|

Monday Morning Quarterback

(Monday, April 22, 2024)

Real estate investors have been busy. I say this because the share of U.S. home sales purchased by investors hit a new high in December, according to CoreLogic data. In October, November and December, the share of single-family home purchases that were made by investors was 28%, 27.3% and 28.7%, respectively. This eclipsed the previous all-time high of 28.3% in February 2022 and makes the investor share rising above 30% in 2024 a distinct possibility. But the connection between price appreciation and investor activity has been inconsistent over the past few years. For instance, in 2019 and 2020, the two metrics always moved in opposite directions, while the intense appreciation of 2021 and 2022 coincided with an unprecedented leap in investor purchases. However, appreciation has since slowed, while the investor share remained high. Elevated interest rates have stymied price appreciation but not investors, and there is no sign that the investor share will fall back to its pre-pandemic level of less than 20% as recorded in the first half of 2023. Indeed, the Federal Reserve has yet to cut rates, and home prices remain high, fueling strong rental demand that investors are seizing upon. The sizable home investor share masks what it really a cold market. Investor purchases are strong only compared with owner-occupied purchases. Investors made 92,000 house purchases in October 2023 before backing off to a respective 80,000 and 79,000 properties in November and December. These numbers are comparable to those recorded in 2022, 2020 and 2019, which show that the true investor surge was in 2021 and that the investor share now is more a sign of investor resiliency to high interest rates than owner-occupied buyers. In other investor news, let’s get under the hood…

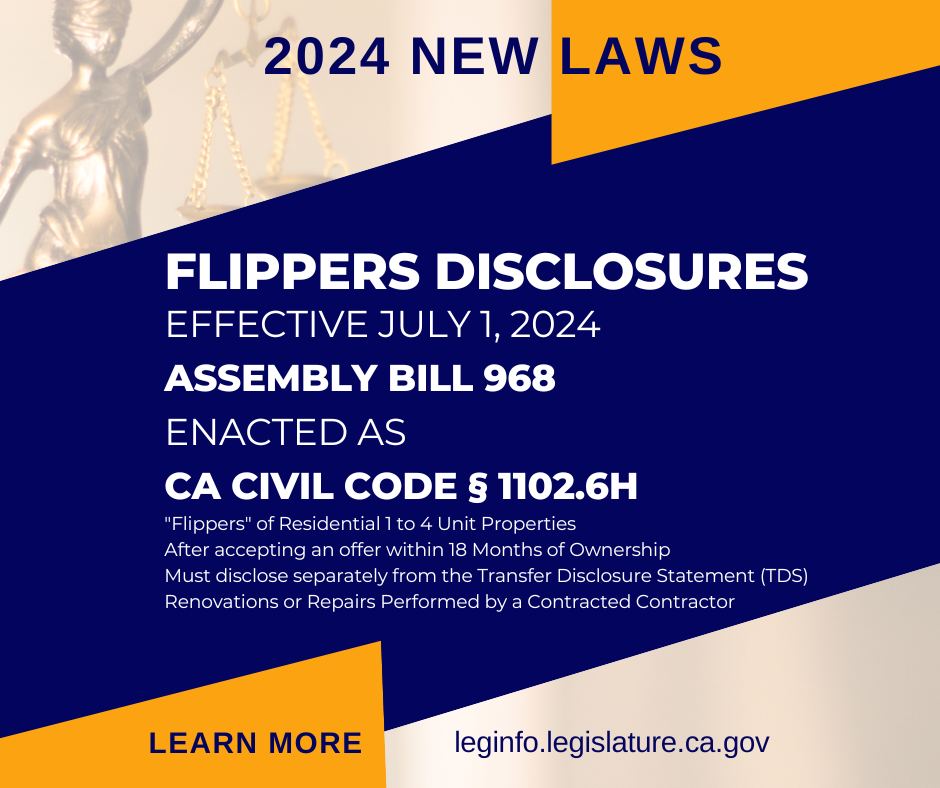

Assembly Bill No. 968 (effective July 1, 2024) Marks A Significant Shift In Real Estate Transactions For Residential Flippers. This new legislation mandates comprehensive disclosure of repairs and renovations by investors who flip properties within 18 months of acquisition. Which means you, Mr. Flipper! The intent is to ensure transparency and protect buyers from undisclosed property conditions:

· New Disclosures. AB-968 requires sellers of single-family residential properties to disclose, among other things, any room additions, structural modifications, and other alterations or repairs made since acquiring the property. This disclosure must include the name of each contractor involved and a copy of any related permits. If permits are unavailable, the seller must guide the buyer on how to obtain them from relevant third parties.

· What is the impact? For residential flippers, this law introduces additional due diligence and documentation responsibilities. They must now meticulously track and report all property changes, including minor repairs, ensuring that all work is properly permitted and recorded. This adds a layer of complexity to the flipping process, potentially affecting the speed and profitability of these transactions.

· What are the legal implications? Failing to comply with AB-968 can lead to legal disputes and financial penalties. Buyers who discover undisclosed work post-purchase may have grounds for legal action, including rescission of the sale or claims for damages. Therefore, investors must understand and adhere to these new requirements fully.

AB-968 significantly affects the dynamics of residential flipping by enforcing stringent new disclosure requirements. Flippers need to be proactive in understanding and integrating these obligations into their business models to avoid legal pitfalls.

|

|

|

Generational Housing Gap. When young parents say buying a house in Los Angeles is becoming increasingly impossible, they’re not exaggerating. New federal data shows they’re right. No American city shuts millennials with kids out of homeownership more than L.A. Millennial parents in Los Angeles own less than 10% of family-sized homes — those with at least three bedrooms. Instead, large homes in L.A. are two-and-a-half times more likely to be owned by empty nesters in the baby boom generation. That’s according to a recent report from Redfin. Researchers analyzed U.S. Census data and found that 23.7% of L.A. metro area homes with three bedrooms or more are owned by people aged 58 to 76 with no children at home. In contrast, parents aged 26 to 41 own just 9.4% of those L.A. homes. “The gap is so pronounced in Los Angeles because the supply shortage is so pronounced,” said Daryl Fairweather, Redfin’s chief economist. “Because of the scarcity, it's like if a baby boomer is occupying a home, that’s one less home that a millennial with kids could occupy.” Of course, this divide exists nationwide. Yes, but the Redfin study reveals that young parents in L.A. are faring the worst. They’re even less likely to own a family-sized home than their peers in cities like San Francisco and New York, where millennials with kids own 10.9% and 11.8% of large homes respectively. These statistics raise a high-stakes question: Why aren’t older homeowners downsizing? When their kids grow up and leave home, why aren’t baby boomers in L.A. selling their houses to families who actually need the space? “The number one reason why people don't move is just inertia,” economists believe. Plus, skyrocketing home values mean few millennials can afford to buy a house today. Sure, some are getting financial help from their parents, but not all Angelenos have relatives who can assist with down payments.

Zillow Is Worried About America’s Housing Shakeup. Since its founding nearly two decades ago, Zillow has revolutionized the way Americans buy, rent, sell (and fantasize) about housing in the US. But a settlement that breaks the grip of powerful real estate agents could trigger a range of problems for the platform already suffering from declining traffic in an increasingly competitive housing market. The company’s stock has dropped nearly 13% since last month’s $418 million settlement between the National Association of Realtors and groups of home sellers (which ended the standard 6% commission for Realtors). It’s a sign that investors fear the settlement could have seismic effects through the housing industry, changing everything from how much Americans pay to buy and sell homes to the income of those in the industry and even the technology underpinning it. Zillow made this point itself in its annual report last month, when the company warned that, “if agent commissions are meaningfully impacted, it could reduce the marketing budgets of real estate partners or reduce the number of real estate partners participating in the industry, which could adversely affect our financial condition and results of operations.” Despite those problems, Zillow still leads in its market. With data on well over 160 million US homes, its residential revenue has outperformed the real estate industry average for six consecutive quarters.

Now the company has hit a crossroads with the NAR settlement and will likely need to adjust its business model accordingly. That’s because one of the main ways Zillow makes money is through lead generation for real estate agents. It offers a product called “Premier Agent” that allows agents to pay to be connected with the customers most likely to purchase homes. Zillow also makes money from agents who pay to have a stronger presence on the site and who pay for AI-enhanced listings, which highlight features that home-buyers in a particular market are most interested in. Nevertheless, the company has been working to find other ways to make money — it has invested heavily in the rental market, which represented 20% of revenue in the second half of 2023. It’s also focusing on home loans, display ads and new real estate software.

|

|

|

New-Home Construction Posts Biggest Drop In Four Years. Construction of new homes fell 14.7% in March, as home builders scaled back new projects. The pace of construction slowed as builders contended with higher mortgage rates sapping demand. Housing starts fell to a 1.32 million annualized pace from 1.55 million in February, the government reports. (That’s how many houses would be built over an entire year if construction took place at the same rate in every month as it did in March.) The drop in March was the sharpest since April 2020, when starts dropped by 27%. Outside of the pandemic, housing starts fell by the most since February 2015. To be sure, new construction has been trending lower in recent months. Housing starts fell in March to the lowest level since August 2023. Building permits, a sign of future construction, also fell 4.3% to a 1.46 million rate. Builders scaled back constructing new single-family homes, leading to a 12.4% drop, as well as apartment starts, which fell 20.8%. New construction fell across most of the nation, with the biggest drops in the Northeast. The West was the only region which saw new construction increase in March. Overall, the drop in new-home construction is a setback for the housing market, which is already facing a housing deficit due to demand outpacing supply. The NAHB estimates that the country is short of roughly 1.5 million housing units. “Restrictive monetary policy has depressed housing activity materially over the tightening cycle,” and that starts are likely to remain around the 1.4 million pace until the Fed eases. Aside from pain points such as the cost to get approvals and develop lots that the builder is facing, homebuyer costs like mortgage rates, insurance, and real estate taxes are adding to the headwinds.

|

|

|

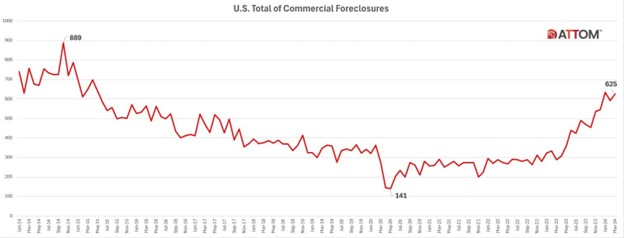

Commercial Foreclosures Increase in March. ATTOM database released an updated monthly report on “U.S. Commercial Foreclosures.” The report reveals a continued increase in commercial foreclosures over the years, from a low of 141 in May 2020 to the current figure of 625 in March 2024. This represents a steady increase throughout the period. In May 2020, the U.S. saw a significant low in commercial foreclosures, hitting 141, reflecting the immediate impacts of the pandemic and swift response measures like moratoriums and financial aid. However by March 2024, commercial foreclosures had risen to 625, a 117% year-over-year increase, compared to the 2020 low. In March 2024, California had the highest number of commercial foreclosures in the country, at 187. This was a 405 percent increase from last year! California began experiencing a notable rise in commercial foreclosures in November 2023, surpassing 100 cases and continuing to escalate thereafter. The usual big-state culprits, New York, Florida, Texas and New Jersey also showed significant variance over the decade, with each state continually increasing. New York had a total of 61 commercial foreclosures in March 2024, a 5 percent increase from last month and a 65 percent increase from a year ago. Then came Florida which saw a 30 percent increase from last month and a 107 percent increase from last year. Texas saw a 31 percent increase from last month and a 129 percent increase from last year. Finally, New Jersey saw a 31 percent increase from last month and a 133 percent increase from last year.

|

|

|

Residential Foreclosure Activity Increases Quarterly in Q1 2024. ATTOM released its Q1 2024 “U.S. Foreclosure Market Report” which shows a total of 95,349 U.S. home with a foreclosure filing during the first quarter of 2024, up 3 percent from the previous quarter but down less than 1 percent from a year ago. The report also shows a total of 32,878 properties with foreclosure filings in March 2024, down 10 percent from a year ago. States that had 100 or more foreclosures starts in Q1 2024 and saw the greatest quarterly increase included, New Hampshire (up 43 percent); Illinois (up 26 percent); Florida (up 22 percent); Rhode Island (up 21 percent); and Nevada (up 16 percent). Major metros with a population of 200,000 or more that had the greatest number of foreclosures starts in Q1 2024 included, New York, New York (4,404 foreclosure starts); Houston, Texas (2,977 foreclosure starts); Chicago, Illinois (2,867 foreclosure starts); Los Angeles, CA (2,398 foreclosure starts); and Miami, FL (2,319 foreclosure starts). Nationwide one in every 1,478 housing units had a foreclosure filing in Q1 2024. States with the highest foreclosure rates were Delaware (one in every 894 housing units with a foreclosure filing); New Jersey (one in every 919 housing units); South Carolina (one in every 929 housing units); Nevada (one in every 961 housing units); and Florida (one in every 973 housing units). Lenders repossessed 10,052 U.S. properties through foreclosure (REO) in Q1 2024, up 7 percent from the previous quarter but down 20 percent from a year ago. States with the longest average foreclosure timelines for homes foreclosed in Q1 2024 were Louisiana (2,641 days); Hawaii (2,031 days); New York (1,958 days); Nevada (1,701 days); and Kentucky (1,701 days). States with the shortest average foreclosure timelines for homes foreclosed in Q1 2024 were Montana (123 days); Virginia (152 days); Texas (163 days); Wyoming (191 days); and West Virginia (217 days).

|

|

|

O.J. Simpson Left Behind an Equally Infamous Property Portfolio. O.J. Simpson, who arguably kicked off the true-crime era with his crazy story (a fascinating brew of salacious gossip, violence, sport, race, and celebrity), died of cancer last Thursday in Las Vegas. Interestingly, real estate played a crucial role in the Simpson saga, in the geographic orbit of the infamous star:

Brentwood, CA. The home at 360 N. Rockingham Drive was where Simpson famously retreated and ultimately surrendered to authorities after a memorable slow-speed car chase. It’s also where he returned following his acquittal. Simpson bought the home in 1977 for $650,000. He and Nicole Brown were married at the luxury property in 1985. Simpson put the five-bedroom home up for auction, selling it back to the bank in 1997 for $2.6 million. Simpson was forced to part with the property after he lost a 1997 civil trial to the families of the murder victims. The $33.5 million judgment against him put Simpson into bankruptcy. It also forced him out of California in an effort to shield his cash from creditors. But if you want a glimpse of the property, you’ll have to scour archival photos. A local investor picked it up for $3.95 million in 1998 and razed the mansion. He even changed the home’s address to reduce any stigma associated with the former football star. It’s now 380 N. Rockingham Drive, and the seven-bedroom home was sold in 2005 for $13.6 million.

Miami, FL. In 2000, Simpson left for the Sunshine State in an effort to preserve his NFL pension from the civil judgment against him. He bought a four-bedroom home in Miami for $575,000. The home at 9450 SW 11t2th Street was foreclosed on in 2012, while Simpson sat in a Nevada prison (after an armed robbery conviction in 2008). Simpson’s Miami home was sold by the bank to a local investor for $513,000 in 2014. In 2023, the home was razed, mirroring the fate of his Rockingham mansion. Today, the vacant property on the city’s south side is on the market for $2.4 million. The 1.65-acre parcel is marketed as the “best priced lot per square foot in the area.”

Las Vegas, NV. After his release from prison in 2017, Simpson opted to stay in the Las Vegas area. A friend of the ex-Bills running back opened up his mansion in a private, gated community near Red Rock Country Club. Simpson didn’t own the place in Summerlin, but he enjoyed the luxury trappings of the five-bedroom home. Highlights of the two-story residence include a backyard putting green, pool, and access to a private golf course. This Las Vegas home was where Simpson died at the age of 76.

Bundy Drive murder site in Los Angeles, CA. The Brentwood townhouse where Simpson’s ex-wife lived (and died) still stands today, albeit with a different address. Nicole Brown Simpson purchased (with O.J.’s assistance) the four-bedroom condo at 875 S. Bundy Drive five months prior to her murder for $625,000. Her home went back on the market in 1995 with a price of $795,000, and it was sold in 1997 for $520,000. The owner changed the home’s facade as well as the address, which is now 879 S. Bundy Drive The home was last sold in November 2006 for $1.72 million.

|

|

|

The Loneliest House in the World. At Ellidaey Island, a windswept speck of land south of Iceland’s Vestmann archipelago, you can leave the world behind and be alone. As it turns out - very alone! This rocky islet of just under two square miles is uninhabited (unless you count its many Puffins) and, thus, there isn’t much infrastructure here. In fact, it seems there’s only a single house. Often spotted by travelers in passing ships, it’s been unofficially dubbed “the loneliest house in the world.” In the 1950s, the Ellidaey Hunting Association built the famous white house as a hunting lodge for its members. Although there are no animals to hunt on the island (unless you consider Puffins wild animals.) While it may have hosted hunters for a few nights, the lodge was never actually somebody’s home. While getting to Ellidaey is no easy feat (generally it’s off-limits for everyday tourists) some adventurers have been granted permission to visit. Videos online show the inside of the lodge, which is decked out in wood paneling, a leather sectional and lounge chairs, as well as plenty of art depicting explorers and other Scandinavian-appearing islands. A number of twin beds line two rooms on the upper level. Once safely at the lodge, you can sign the visitors log, which reportedly captures everyone who has ever set foot inside the house (the tally is up to 11,265). Keep in mind, everything in the house, from the construction materials to the furniture, was brought in by boat, then carried up the steep cliffs, and then lugged to the site of the house. For those of you considering Ellidaey Island as a destination to ride out a zombie apocalypse, it seems you now have a lonely house on a deserted Iceland island to escape to.

|

|

|

Basic Training Investing Boot Camp. Saturday, April 27, 2024, 9:00 am to 6:00 pm, will be our semi-annual Basic Training Boot Camp. Everything you ever wanted to know about real estate investing but were afraid to ask. Iman Cultural Center, South Hall, 3376 Motor Avenue (between National and Palms), Los Angeles, 90034.The cost of the Boot Camp is $149.00 per person if paid before April 20. After April 20, the price jumps to $1 million! So don’t wait to register. (Gold Members and former Boot Campers can attend for FREE, but still need to register.) You can register at LARealEstateInvestors.com.

|

|

|

Vendors Expo Returns! Our world-famous, super-duper "Vendors Expo" returns on Thursday night, May 9, 2024. The Vendor Expo opens starting at 6:30 pm. We'll have 40+ of the finest vendors featuring real estate products and services you will want to utilize as a successful investor. Stick around after and enjoy our guest speaker. Iman Cultural Center, 3376 Motor Avenue (between National and Palms), Los Angeles, CA 90034. FREE Admission. Metered and free street parking. Please RSVP at www.LARealEstateInvestors.com.

|

|

|

You Go Girl! Meet Women Who Rock Real Estate. Join us on Thursday night, May 9, 2024, when we have a very special panel on women investors. Our moderator will be Deborah Razo, President of the Women’s Real Estate Network (“WREN”). Deborah is an all-star investor, including fixing and flipping houses, residential construction, and multi-residential properties in the U.S. and Puerto Rico. The panel will feature Cindy Coleman discussing note investing, Angela Sillmon discussing short-term rentals, and Jen Maldonado discussing raising capital for your projects. The women will be discussing how they started investing and challenges they confronted along the way. If you’re a woman investor, DO NOT miss these talented women! (men, you can attend - but at your own risk!) Iman Cultural Center, 3376 Motor Avenue (between National and Palms), Los Angeles, 90034 (Culver City adjacent). FREE Admission. Metered street parking. RSVP at www.LARealEstateInvestors.com.

|

|

|

“Cash Flow Chronicles” Podcast. We are so very excited about our podcast, "Cash Flow Chronicles" hosted by our very own Bill Gross. Bill has been a Realtor, broker and real estate investor since the Ice Age! No one is more experienced in local Southern California real estate than Bill Gross. Each week, Bill interviews real estate professionals sharing their insights and advice. Every Tuesday at 3:00 pm, and anytime thereafter on YouTube, Facebook, and Google.

This Week. Investors will continue to watch for Fed officials to elaborate on their plans for future monetary policy. They will also keep an eye out for signs of escalation in the conflict in the Middle East. For economic reports, New Home Sales will be released on Tuesday from the Census Bureau. Gross Domestic Product (GDP), the broadest measure of economic activity, will come out on Thursday from the Bureau of Economic Analysis. Personal Income and the PCE price index, the inflation indicator favored by the Fed, will be released on Friday, also from the Bureau of Economic Analysis.

Weekly Changes:

10-Year Treasuries: Rose 010 bps

Dow Jones Average: Fell 100 points

NASDAQ: Fell 600 points

Calendar:

Tuesday (4/23): New Home Sales

Thursday (4/25): Gross Domestic Product

Friday (4/26): Core PCE

For further information, comments, or questions:

Lloyd Segal President

Los Angeles County Real Estate Investors Association This email address is being protected from spambots. You need JavaScript enabled to view it.

310-792-6404

|

|

|

|