|

Monday Morning Quarterback

(Monday, January 22, 2024)

Housing Outlook for 2024? This year I expect modest gains all around: modest gains in housing starts, modest gains in sales, and modest gains in prices. A recession, by itself, would have a negative effect on housing. But there are so many other factors affecting housing that most economists think our sector will weather the economic storm. In terms of construction, builders started fewer homes in 2023 than in 2022, which was already down from the COVID peak in 2021. But builders have been consistently building too few homes since the bursting of the housing bubble over fifteen years ago. As a result, economists expect a turnaround in 2024. However, the gains will be concentrated in single-family homes; the number of multi-family homes (think apartments and condos) under construction is at an all-time high already. In terms of sales, it will be hard for the existing home market to get any worse in 2024. Sales have been handcuffed in 2022-23, for two reasons. First, temporary indigestion as mortgage rates rose. Second, homeowners who borrowed money at rock-bottom mortgage rates in 2020-21 have been very reluctant to sell. After all, who in their right mind would give up a mortgage with a fixed rate of something like 2.75% locked in for fifteen or even thirty years? But with each passing year a gradually smaller share of homeowners will be locked in with those rock-bottom mortgage rates. Some of them must move anyhow, for one reason or another. In addition, mortgage rates should be lower this year than in 2023, helping boost sales among prospective buyers and sellers. Meanwhile, new home sales were up in 2023 and should continue to grow in 2024. Lower mortgage rates should help a little, as will the construction of more single-family homes. The biggest surprise in the housing market last year was that prices increased consistently after falling in the second half of 2022. Through the first ten months of 2023, the national Case-Shiller Index and the FHFA Index were both up roughly 6.0%. I think the continued resilience of home prices largely reflects a lack of supply. However, a faster pace of construction in 2024 should establish a ceiling on price gains in the year ahead. Put it all together and we have a recipe for general improvement in housing even as the rest of our economy slows down. In other real estate investor news, let’s get under the hood…

Housing Starts Declined in December. Housing starts declined 4.3% in December to a 1.460 million annualized rate. The drop in December was entirely due to single-family starts. In the past year, single-family starts are up 15.8% while multi-unit starts are down 7.9%. While the data have been choppy, it seems that developers may have finally found their footing as we closed out the year in what had been a challenging environment for sales. This likely has to do with the move in mortgage rates, driven by the widely held belief that the Federal Reserve will cut short term interest rates multiple times in 2024. While 30-year mortgage rates remain right around 7%, they have been on a downward trajectory since peaking above 8% at the end of October. Economists expect mortgage rates to continue trending downward in 2024, providing a tailwind for activity. Looking at the details of the report, housing starts declined 4.3% in December, yet still beat consensus expectations. Building permits also beat consensus expectations, rising 1.9% to a solid 1.495 million annual rate. The gain was due to permits for both single-family and multi-unit homes. While multi-unit permits have been trending down over the past year, permits for single-family homes have increased in each of the last eleven months. Meanwhile, housing completions surged 8.7% in December to a 1.574 million annualized rate. In 2023, an estimated 1.452 million housing units were completed, 4.5% above the 2022 figure of 1.391 million, but still below what we need to keep up with population growth and scrappage of old homes. In the past year, the number of single-family starts is up 15.8% while multi-unit starts are down 7.9%. This huge gap in the data is due to the unprecedented nature of the last three years since COVID began. While economists don’t see housing as a major driver of economic growth in the near term, recent numbers are certainly not what you’d expect to see if there was a severe housing bust like the 2000s on the way, either.

|

|

|

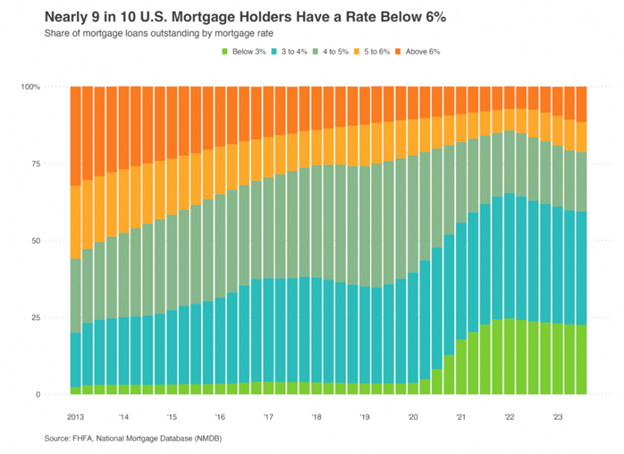

89 Percent Of People With Mortgages Have Interest Rate Below 6 Percent. The “lock-in effect” is real. And it’s strong. According to Redfin, 88.5 percent of U.S. homeowners with mortgages have an interest rate below 6 percent, down from a record high of 92.8 percent in 2022. A big reason for the drop is, of course, the fact that everyone who purchased a home in the last year was entering the market at a time when the average mortgage rate was above 6 percent. But it also speaks to the inventory shortage, as many would-be sellers wait out the market for interest to further fall. Here’s the full breakdown of where today’s homeowners fall on the mortgage-rate spectrum:

· Below 6 percent: 88.5 percent of mortgaged U.S. homeowners have a rate below 6 percent, down from a record 92.8 percent in the second quarter of 2022.

· Below 5 percent: 78.7 percent have a rate below 5 percent, down from a record 85.6 percent in the first quarter of 2022.

· Below 4 percent: 59.4 percent have a rate below 4 percent, down from a record 65.3 percent in the first quarter of 2022.

· Below 3 percent: 22.6 percent have a rate below 3 percent, down from a record 24.6 percent in the first quarter of 2022.

|

|

|

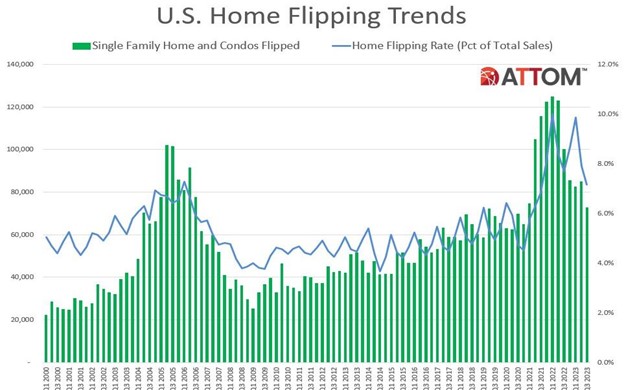

Home Flipping Keeps Falling In Third Quarter Of 2023. ATTOM released its third-quarter “2023 U.S. Home Flipping Report” showing that 72,543 single-family homes and condominiums in the United States were flipped in the third quarter. Those transactions represented 7.2 percent (or one of every 14 home sales nationwide), during the months running from July through September of 2023. The latest portion was down from 7.9 percent of all home sales in the U.S. during the second quarter of 2023. While the flipping rate remained historically high, it dropped for the second straight quarter, to the lowest point in two years. But even as flipping rates declined, the latest analysis also reveals that fortunes continued improving for home flippers during the third quarter in the form of rising profits. Investor returns increased for the third quarter in a row, rebounding from a slump that had slashed profit margins by nearly two-thirds from early-2021 to late-2022. Margins, along with raw profits, rose to the highest levels since the middle of last year. The typical third-quarter profit margin of 29.8 percent nationwide (based on the difference between the median purchase and median resale price for home flips) remained far below peaks hit in 2021. But it was up from 29 percent in the second quarter of 2023 and up seven percentage points from a low of 22.4 percent in the fourth quarter of last year. Raw profits on typical flips around the country, meanwhile, increased to $70,000. That remained well down from a high of $110,000 reached in 2021. But it was up slightly from the second quarter of 2023 and was $15,000 more than last year’s low point. Among those metros, the largest flipping rates during the third quarter of 2023 were in Macon, GA (flips comprised 16.1 percent of all home sales); Salisbury, MD (14.1 percent); Spartanburg, SC (13.3 percent); Atlanta, GA (13.2 percent) and Fayetteville, NC (12.8 percent).

|

|

|

Typical Home In These Cities Will Be Worth $1,000,000 Within 10 Years. The housing market is already unaffordable in many parts of the U.S., but in these California cities, the typical home is expected to be worth more than a million dollars within the next 10 years. The analysis from Zillow looked at home values over the next decade. Economists at the company said they used a “fairly conservative” method that blended their short-term forecast and historical average for each market, and found that four California cities would have typical homes worth more than $1 million a decade from now. The most-expensive cities ten years from now are commonly known as expensive, high-cost metros: San Diego, San Francisco, San Jose, and Los Angeles. Homes in San Francisco and San Jose are already worth more than $1 million today. The other two cities currently have a typical home value of less than $1 million, according to Zillow’s data. But a decade from now, the typical home in San Jose would be around $1.5 million, the most expensive in the nation, Zillow found, followed by San Francisco, at $1.19 million, and San Diego, at $1.09 million. A typical home in Los Angeles a decade from now would be about $1.05 million. “The housing shortage is the biggest reason home values have risen so much over the past decade, and why they are expected to continue to rise,” Nicole Bachaud, senior economist at Zillow says. The U.S. is short of at least 2.3 million homes, according to an estimate by Realtor.com. Over the last year, despite a surge in mortgage rates, housing demand continues to outstrip supply and home values rose to an all-time high. One of the big drivers of home prices is the low supply of homes. With few homeowners interested in selling their homes, that keeps a lid on the number of resale listings. After all, homeowners see little incentive at the current moment to sell, as they would need to give up their low mortgage rate in the 3% to 4% range (or even lower for a 30-year mortgage rate in the 6% or even 7% range). No thank you, they say. A lack of newly built homes will also push home prices up over the next decade, Bachaud added. “We are in a construction boom, which is good news, but recent Zillow research has shown we are 4.3 million homes short of what we need,” she said. “It’s important this construction boom continues into the coming years.” Strong demand from home buyers will also pressure prices up.

|

|

|

New California Housing Laws Streamline Building Process In 2024. If California wants to build its way out of its long-term housing shortage, plenty of things stand in its way in 2024: high interest rates, sluggish local approval processes and a persistent shortage of skilled construction workers, among others. But a slew of housing bills from the 2023 legislative session effective January 1 promise to ease or eliminate some of the other burdens. Among the batch of fresh housing laws are an especially high profile set by San Francisco Democratic Senator Scott Weiner: Senate Bill 423 re-ups and expands a law that speeds up the approval of apartment buildings in which some units are set aside for lower income Californians, while SB 4 does something similar for affordable housing on property owned by religious institutions and non-profit colleges. Wiener’s two new laws set the tone of housing legislation in 2024, where ripping out barriers and boosting incentives for housing construction emerged as the dominant theme. “The era of saying no to housing is coming to an end,” Wiener said in a statement after the two bills were signed. That was especially true for developers of purpose-built affordable housing, per policy analysts at UC Berkeley’s Terner Center for Housing Innovation in an end-of-year legislative summary. Lawmakers, the analysts wrote, in the continuation of a “remarkable run over the last several years,” gave “more flexibility to exceed or override local zoning, greater certainty on the timing and likelihood of planning approvals, and substantial relief from (environmental) review and litigation.” “I am deeply concerned about the market and how few young buyers can actually afford to get into the game anymore,” said Seth Phillips, founder of the Los Angeles-based development and consulting firm ADU Gold (and previous speaker at LAC-REIA). “If they do it right, if they really get the processes right…young homebuyers could have a whole bunch of new stuff to pick from, which basically doesn’t exist right now.”

|

|

|

Nation’s Largest Single-Family Home Landlord To Pay $3.7 Million Penalty. Landlords do not, I repeat do not, raise rents in violation of California’s rent caps. I mention this because the nation’s largest landlord of single-family home rentals will pay $3.7 million in civil penalties and restitution to resolve allegations it violated California laws against rent gouging, state Atty. Gen. Rob Bonta announced last week. Between October 2019 and December 2022, Invitation Homes (which owns 12,000 properties in California), increased rents for 1,900 tenants above the allowable amounts per state laws. (The California laws limit annual rent increases to 5% plus a regionally adjusted inflation figure, but no more than 10% overall.) Under a proposed settlement filed in Los Angeles County Superior Court last week, Invitation Homes will pay $2.04 million in penalties. The company is spending an additional $1.68 million to refund tenants the amount it collected in excess of the state’s rent cap plus 5% interest. Signed by Governor Newsom in 2019, California’s rent cap law has been one of the highest-profile responses to the state’s housing affordability problems. The law, one of the strictest limits on rent increases in the country, applies to all multifamily rental housing except for apartments built within the last 15 years. The law covers single-family home rentals operated by corporations or institutional investors such as Invitation Homes but exempts some other properties. Currently, under the law, landlords are allowed to increase rents by no more than 8.8% in Los Angeles and Orange counties, 9.2% in the Bay Area and varying figures elsewhere in California. It affects properties built before 2008. Some California cities, such as Los Angeles and San Francisco, have local rent control policies that more tightly limit rent increases in older buildings. Invitation Homes operates 85,000 properties across the country. Its 12,000 units in California account for 17% of the company’s $614 million in rental revenue during the three months that ended Sept. 30. The $2,982 average monthly rent for Invitation Homes properties in Southern California is the highest in its nationwide portfolio, the report said.

|

|

|

Trouble Piles Up As NAR Faces Extinction-Level Events. Zillow is suing multiple listing services across the United States, accusing them of forcing Zillow’s listing service out of business in order to maintain illegal monopolies. The lawsuit represents another blow to established residential real estate players, including the beleaguered National Association of Realtors. The lawsuit, filed Dec. 22 in an Arizona federal court, says Seattle-based Zillow’s home tour scheduling platform “ShowingTime” is being forced out by multiple listing services, including the Arizona Regional Multiple Listing Service, the Milwaukee-based Metro Multiple Listing Service and MLS Aligned, a collective owned by six listing services. Zillow alleges a violation of federal antitrust laws and an attempt by multiple listing services (many of them NAR-affiliated), to secure a monopoly. The challenge to NAR and other prominent real estate organizations follows an October decision to award $1.8B to home sellers after a jury found that NAR and several large residential brokers conspired to artificially inflate real estate commissions. It also comes as the NAR reels from sexual harassment allegations against former President Kenny Parcell that led to his resignation last year and as it fends off more than 10 lawsuits, The New York Times reports. The organization is facing bankruptcy, according to the NYT. Amid a Justice Department investigation of NAR for antitrust violations, large brokerages like Re/Max and Coldwell Banker no longer require agents to maintain NAR memberships. Redfin requires some agents to stop paying dues after it cut ties last year. Together, the moves could equate to a death blow for the organization that trademarked the term “Realtor,” the NYT reports. In fact, several high-profile real estate agents are talking about starting their own groups if NAR goes under. Real estate mogul and reality TV star Mauricio Umansky is one agent laying the groundwork to start an alternative association, according to the NYT. Similar to the Zillow lawsuit, Umansky is suing NAR after it tried to shut down his private home listings site.

Chicago’s Great Lake Jumper Does It Again Despite Below-Zero Temps. While Southern California “suffers” through sub-70 temperatures, meteorologists are warning Chicagoans to stay inside this weekend amid the dangerously cold, below-zero temperatures and dress in multiple layers if they venture outside. But Dan O’Conor is not having it. The city’s famed “Great Lake Jumper” dove into Lake Michigan once again yesterday morning (despite the negative-7 degree air temperature, negative-25 wind chill and sub-freezing water). O’Coner, along with friends Molly Kavanaugh and Glenn Rischke, took the plunge at Montrose Harbor, continuing O’Conor’s more than three-year streak of starting the day, every day, in the lake, despite the weather. Actually, O’Conor has been jumping into Lake Michigan every day since June 2020, when he woke up hungover and decided to head to Lake Michigan to clear his head. It was a Saturday and O’Conor said he had been stressed since COVID-19 first hit Chicago. Every day, while the news had updates on a pandemic with seemingly no end in sight. O’Conor rode his bike to the lake, locked it up and walked along the wall facing Lake Michigan near Montrose Harbor. On a whim, he said, he dove in. “It was so enjoyable. I just kept doing it,” O’Conor said. “Going down there every day and having some peace of mind when I jumped in. It’s almost meditative.” O’Conor is an artist who lives in Lincoln Square and runs a clothing company called Dtox Designs. Over the past three years, he’s drawn crowds to watch him jump, had bands play at the lake as he goes in and dedicated plunges to lost friends and icons. More than 1,200 times now, the 56-year old O’Conor has propelled, somersaulted, or cannonballed his body into Lake Michigan.

|

|

|

Motherly Love. According to the Guinness World Records, the greatest officially recorded number of children born to one mother is 69. Yes, 69 children! This remarkable feat was achieved by a Russian woman named Mrs. Vassilyeva, who gave birth to 16 pairs of twins, seven sets of triplets, and four sets of quadruplets between 1725 and 1765. It's an astonishing record that has stood for centuries, highlighting the incredible potential of human reproduction.

|

|

|

How to Invest in Airbnb Short-Term Rentals. Matt Floyd and Craig Gerulski started just like you. They attended the San Diego’s Outback RE meetup back in 2020 and decided to work together. Since then they have built a seven-figure short-term rental business with a portfolio of 30 properties under management, 5 rental arbitrage units and six short-term rental properties in San Diego, Nashville and Scottsdale. And they continue to grow, now negotiating to leverage their expertise to acquire hotels around the country. And the best news of all is that you can do it too! Don’t miss Matt and Craig's presentation. Thursday night, February 8, 2024, 6:30 to 9:30 pm. Plus, come early and enjoy our Vendors Expo. Iman Cultural Center, 3376 Motor Avenue (between National and Palms), Los Angeles, 90034. FREE Admission. RSVP: LARealEstateInvestors.com.

|

|

|

Vendors Expo Returns! Our world-famous, super-duper "Vendors Expo" returns on Thursday night, February 8, 2024. The Vendor Expo opens starting at 6:30 pm. We'll have 40+ of the finest vendors featuring real estate products and services you will want to utilize as a successful investor. Stick around after and enjoy our guest speaker. Iman Cultural Center, 3376 Motor Avenue (between National and Palms), Los Angeles, CA 90034. FREE Admission. Metered and free street parking. Please RSVP at www.LARealEstateInvestors.com.

|

|

|

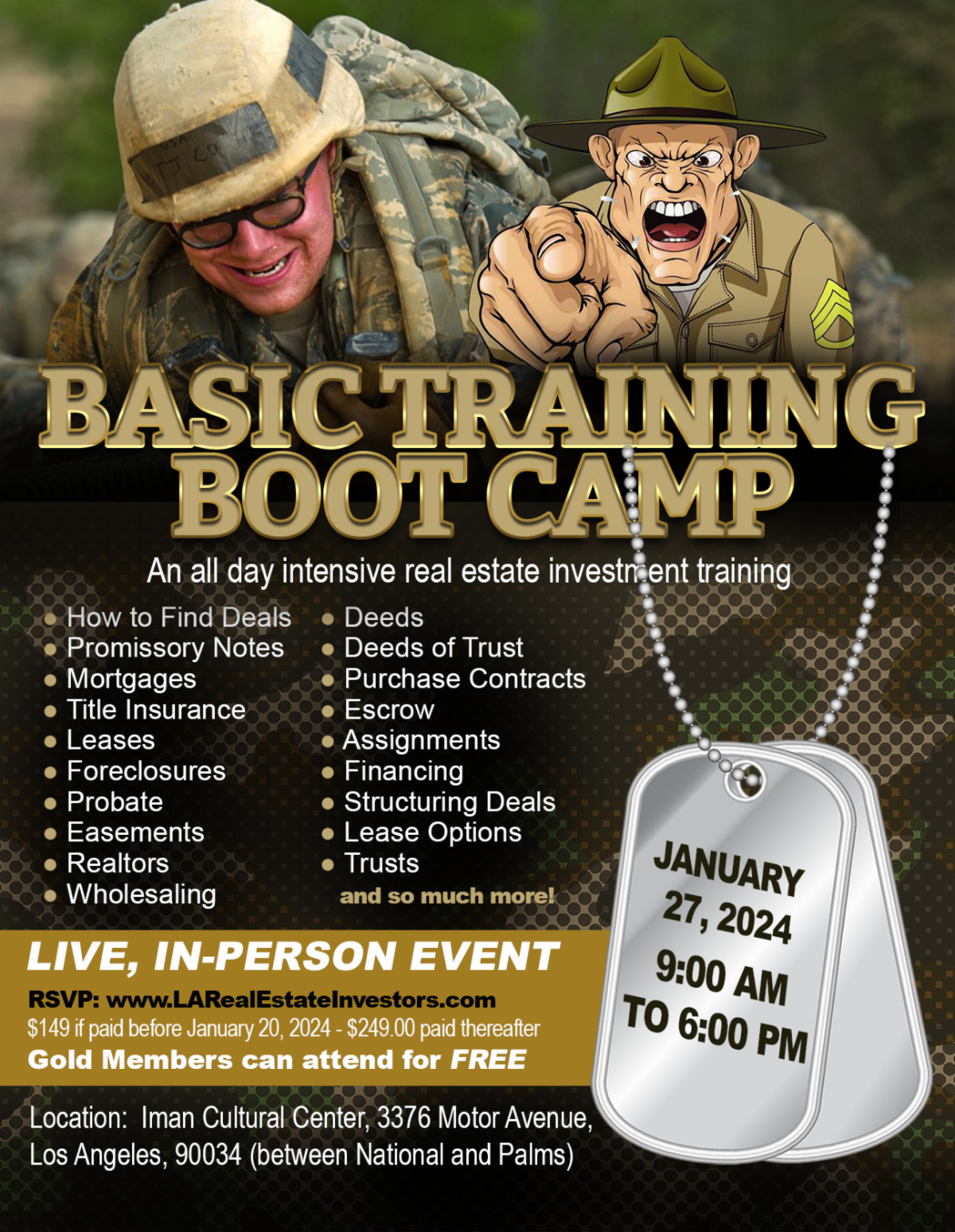

Basic Training Investing Boot Camp. Saturday, January 27, 2024, 9:00 am to 6:00 pm, will be our semi-annual Basic Training Boot Camp. Everything you ever wanted to know about real estate investing but were afraid to ask. Iman Cultural Center, South Hall, 3376 Motor Avenue (between National and Palms), Los Angeles, 90034.The cost of the Boot Camp is $249.00 per person. So don’t wait to register. (Gold Members and former Boot Campers can attend for FREE, but still need to register.) You can register at LARealEstateInvestors.com.

|

|

|

|

This Week. Investors will continue to watch for Fed officials to elaborate on their plans for future monetary policy. For economic reports, New Home Sales and Gross Domestic Product (GDP), the broadest measure of economic growth, will be released on Thursday. Personal Income and the PCE price index, the inflation indicator favored by the Fed, will come out on Friday. The next Fed meeting will take place on January 31.

Weekly Changes:

10-Year Treasuries: Rose 020 bps

Dow Jones Average: Fell 100 points

NASDAQ: Rose 100 points

Calendar:

Thursday (1/25): Gross Domestic Product

Thursday (1/25): New Home Sales

Friday (1/26): CORE PCE

For further information, comments, and questions

Lloyd Segal

President

Los Angeles County Real Estate Investors Association, LLC

www.LARealEstateInvestors.com

This email address is being protected from spambots. You need JavaScript enabled to view it.

310-409-8310

|

|

|

|